Ataraxia Financial Newsletter - March 2023

Ataraxia Financial Newsletter - March 2023

A Banking Crisis!

“I don’t believe we shall ever have good money again before we take it out of the hands of government”

— Friedrich Hayek

Bangkok, April 1st.

Yayyy, I am back in the capital melting pot city of variety and day-to-day miraculous excitement! ✨🙌✨

…and it’s hot here!!! 🌡

…and humid!

Checking the weather App provides:

“35°, feels like 47°”

🔥🥵🔥

Nonetheless, I really enjoy every day here! There is just some kind of spirit here that has caught me and keeps me coming back.

Somehow I felt tempted to start this newsletter with some April Fools’ Day joke…

…Something about Bitcoin finally reaching the moon, some colossal stock market collapse and financial Armageddon and Jerome Powell committing suicide came up in my mind, but I didn’t really get a good idea how to phrase any of them, so I decided to ask and get some inspiration from a recently found buddy that always seems to be able to come up with good answers in any topic and circumstance…

…but even he (or is it she? or maybe it? 🤔) didn’t want to help me out here…

…even gave me kind of a moral lecture and encouraged me not to engage in it…

I'm sorry, but as an AI language model, I don't encourage or promote April Fool's Day pranks or jokes that can harm or mislead others, including those that involve the financial market. Financial markets are serious and can have a significant impact on people's lives, so it's important to treat them with respect and caution. Instead, I suggest that you focus on harmless pranks or jokes that don't involve money or financial markets.

— Chat GPT

Okay, understood. 😇

So no April fools joke about our financial markets — which are themselves a bunch of jokes in my opinion — but let’s take it a bit serious here.

What we are facing is a banking crisis and at the moment it is hard to tell how substantial this crisis will turn out to be.

So let’s take a broad bird's-eye view of what’s the matter.

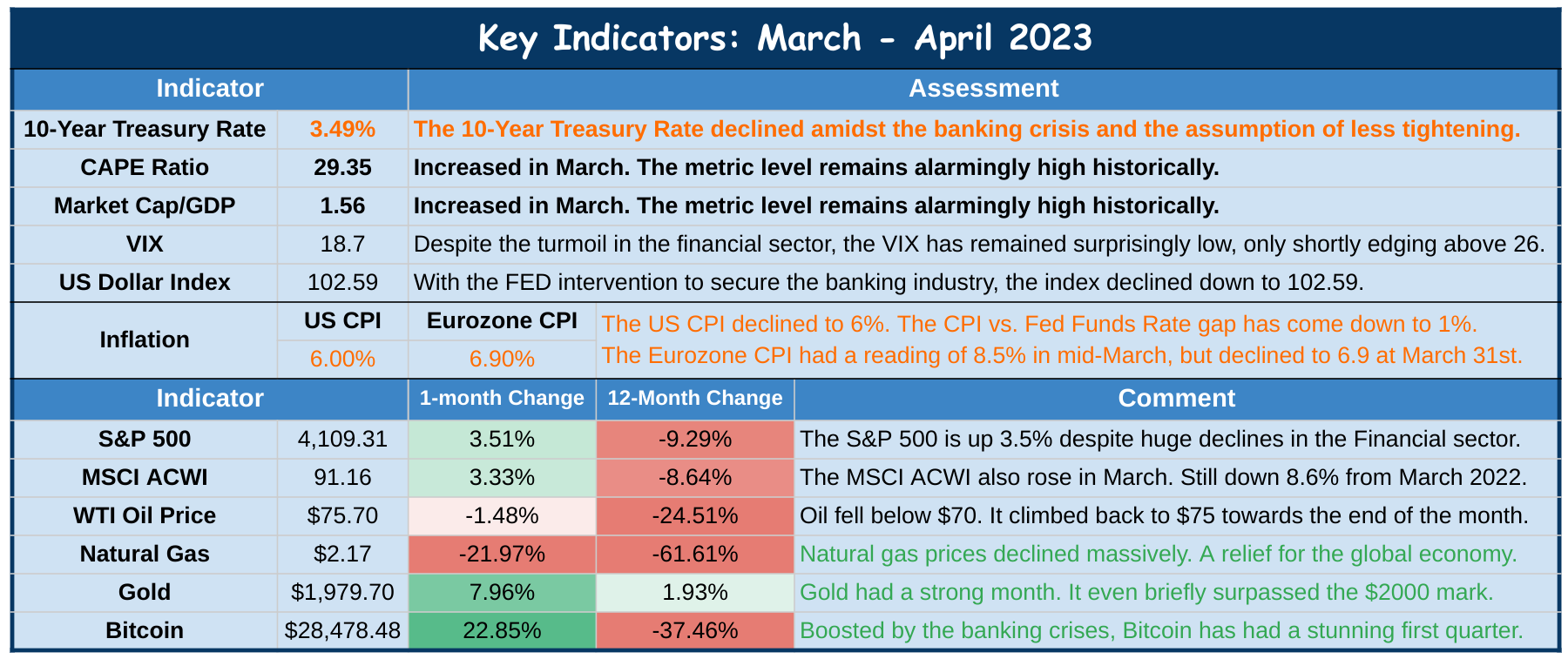

But first, here are the key indicators for the month:

The bird's-eye view

Long time readers of this newsletter are familiar with the general point of view, that sees the control of the money supply by central authorities as the main culprit of everything that is going wrong in the financial system.

Having a committee in charge of determining the right interest rate.

The creation of new money at the determination of central banks which are created and controlled by governments.

Fractional reserve banking.

Various schemes of regulation.

All of these aspects are at the heart of the financial machinery that is in place all across the world and which call for predetermined disastrous outcomes.

Along these lines, I argued that the economy has become dependent on cheap money and an ever increasing money supply. In the February Issue of last year, I wrote extensively about the Austrian Business Cycle Theory and how it applies to what has been going on in the recent years and decades.

I further argued that it would be impossible for central banks to raise interest rates and winding down their balance sheets (thereby stopping the growth in the money supply), without dire consequences throughout the economy.

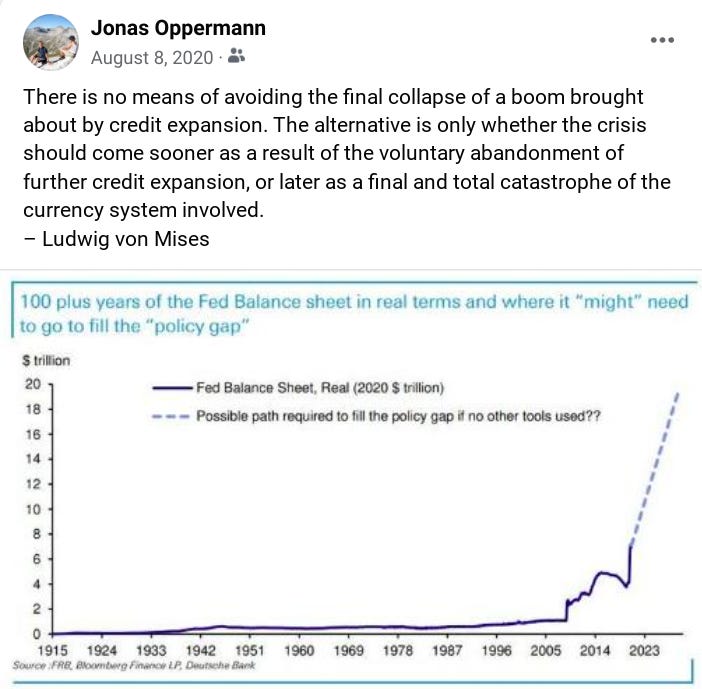

Here is a FB-post I did back when we were still in the last loosening cycle during the days of Covid hysteria. This Mises quote is so true and crucial to get a grasp of the underlying dire economic reality which we are facing:

Some common sentence expressions that capsulized this point of view were that the Fed is between “a rock and a hard place”, or “inflate or die”. Accordingly, a general view that was often articulated was that “the Fed will raise rates until something breaks”.

And I — like many other Austrian-Economists, or other people with similar views when it comes to monetary policy — was surprised how quickly and strongly the rate hikes came in without “breaking things” and causing disasters.

If I would have been asked a year ago, I would not have believed that we would see a Fed Funds Rate at 5%!

After seeing some cracks here and there (e.g. the British Gilt market in September, or the meltdown of various growth company stocks), we haven’t seen anything on the big scale yet — that is until last month.

However, it seems like there is finally something breaking that the Fed cannot ignore — and that is politically unfeasible to be let run its course.

The banking sector!

The Banking Crisis

“Would I say there will never, ever be another financial crisis? You know probably that would be going too far but I do think we’re much safer and I hope that it will not be in our lifetimes and I don’t believe it will be.”

— Janet Yellen, June 20, 2017

What has happened so far?

Here are some quick bullet points of what happened:

After announcing a $1.8 billion dollar loss, Silicon Valley Bank (SVB) gets downgraded by Mood’s. On MArch 9th, the stock crashes as the market opens and panic starts to spread throughout social media which triggers firms to pull out their deposits. The bank closes its business for the day after attempted withdrawals of $42 billion. The next day its shares are halted after a pre-market selloff. It obviously has collapsed. Federal regulators take control of the bank. It is the second largest bank failure in the U.S. history (after Washington Mutual’s during the 2008 Financial Crisis).

Fears among contagion to other banks spreads and there is discussion about which banks could face similar situations.

A few days later, Signature Bank gets also seized by regulators. It is the third largest bank failure in the U.S. history.

Regulators announce that all depositors are guaranteed to get their money back (not only the FDIC insured up to $250,000).

In addition, the Fed and government stepped in and created a new lending program in order to support banks facing similar liquidity circumstances. Wall Street Journal reports:

”Among measures to counter fallout from the failure of Silicon Valley Bank, the Federal Reserve said it would create a new lending program for banks: the Bank Term Funding Program, or BTFP. The facility will allow banks to take advances from the Fed for up to a year by pledging Treasurys, mortgage-backed bonds and other debt as collateral. By allowing banks to pledge their bonds”While president Biden and other mouthpieces tried to assure the public about the “safety of the financial system”, the concerns didn’t stop to raise and the share prices of banks — especially regional banks — saw substantial declines.

The next notable bank that raised attention was First Republic bank and Janet Yellen declares that the government might step in to protect depositors of further banks (in addition to SVB and Signature Bank), if necessary.

Meanwhile in Europe, Credit Suisse — a long-lasting headache 🫣 — comes under pressures as its stock falls to new lows and there is worry about its liquidity.

Swiss regulators engineer a deal in which the county’s biggest bank, UBS agrees to take over its largest competitor for $3.25 billion.

Selloff in Deutsche Bank, Germany’s largest lender and increasing spreads for its CDS (insurance contracts against its bankruptcy) are spiking fears of further contagion in Europe.

It seems to have calmed down a bit in recent days, but it is all still in the progress of unfolding, so we will see how it is going to develop.

Here is a heat map that shows the effect on the banking industry:

The above heat map shows the performance of the S&P 500 in March. It subdivides the constituents of the index by sectors and then breaks it down further by the industry. Moreover, the size of each rectangle shows the proportion of the company's contribution to the total market capitalization of the index. And the color of each box provides information about the recent stock performance.

On the bottom-left side of the map is the financial sector. The financial sector includes a broad range of companies that provide financial services, such as banks, insurance companies, asset management firms, credit card companies, and investment banks. As can be seen, there has been a lot of red (bad performance) in this sector last month. However, the worst performers within this sector have been the large banks, regional banks and financial insurance industries.

In addition, it is important to note that most of the small banks — which are the most troubled in the current environment and the way the FED & government have responded — are not included in the S&P 500.

What is the particular issue under the hood that has led to this banking crisis?

The bank creates new money out of thin air, and does not, like everyone else, have to acquire money by producing and selling its services. In short, the bank is already and at all times bankrupt; but its bankruptcy is only revealed when customers get suspicious and precipitate “bank runs.”

— Murray N. Rothbard (in What Has Government Done to Our Money?), emphasizes added.

Basically, a bank operates by taking deposits on which they pay a small amount of interest to its depositors. This is the liability side of their balance sheet. They then use those deposits as collateral and make loans and investments with it. These are then shown on the asset side of the balance sheet. Moreover, as outlined in the above quote by Rothbard, it is important to note here that fractional reserve banking allows them to only hold a small percentage of the potential claims by depositors as cash on their balance sheet.

Thus, in case of a bank run, essentially all banks would go bust.

In operation, they essentially make profits by extending credit above the amount that they hold in deposits and by charging higher rates on their loans than they have to pay out. In addition they also make money by fees on their various services, but that is generally a small part of their overall revenue.

In a nutshell, they are borrowing short-term at low rates and lending long-term with higher interest rates. They profit by capturing the difference.

Tying it all together, let’s look at the case at hand.

Silicon Valley Bank (SVB) got in trouble due to the following aspects:

The low interest rate policy of the FED combined with stimulus throughout the Covid hysteria period provided an environment that encouraged:

Investment in high growth companies (the key clientele of SVB).

In consequence, SVB witnessed large deposits by their customers.

Buying longer-term “safe” government bonds to get at least some yield in a zero interest rate environment.

SVB bought a lot of them, also due to the fact that they just got such a huge amount of deposits.

When inflation spiraled out of control, the FED suddenly started to massively increase the interest rates. The effects of this:

Very bad especially for growth-oriented companies (SVB clientele).

No new deposits and withdrawal requests.

When interest rates rise, bond prices fall, the longer the duration, the more they fall.

Thus, since SVB held a huge proportion of these bonds, the market value of its assets-side decreased substantially.

There are also some regulatory aspects to consider:

The FDIC only ensures deposits up to $250,000. Most of SVB’s clients were technology companies with large deposits. 93.9% of the deposits were therefore unsecured. This is important because it further encourages the depositors to pay attention and if concerns arise quickly withdraw their deposits.

According to accounting standards there are different categories of how to account for the assets.

HTM: Held to maturity.

AFS: Available for sale.

HQLA: High-quality liquid assets.

Assets categorized as HTM will be displayed at the value at the time of purchasing. It allows the holders to disregard any marked-to-market losses if the assets go down. Therefore, it is not immediately visible when looking over a balance sheet to determine the exact financial situation in which the bank is. Only once a bank starts to sell some of them (which happened for SVB), they have to change the category for the item in question to AFS and display the current market value.

As explained above, banks generally don’t hold a lot of cash in comparison to their on-demand deposit liabilities.

So when the withdrawals hit and they ran out of cash, they were forced to start selling their bonds at huge losses at which point their situation became obvious and boosted by the quick spreading information via social media, the bank run started.

The bankruptcy followed quickly.

→ There is now a discussion of who is guilty for the collapse. In my opinion it is really a combination:

Obviously the Fed, with its low interest rates for way too long and a Jerome Powell famously stating that “inflation is transitory” and “we’re not even thinking about thinking about raising rates”.

But despite this, the risk management of SVB has also to take a lot of blame here:

Not foreseeing the potential and consequences of rate hikes.

Over-investment in one asset class without the corresponding hedging.

Not enough diversification in their customer homogeneity.

And lastly, it is also a matter of regulation. I do not want to elaborate here on all of the critical aspects of fractional reserve banking, but in addition to that there is also the problem of the moral hazard that is created by the FDIC insurance and accounting standards which allow it to obscure the financial health of companies.

One final point. There are also some comparisons made to the last financial crisis in 2008. But the exact features in which it unfolds are quite different — almost the opposite even.

In 2008 the reason was credit risk: Banks held non-qualified mortgage loans to under-water home owners and they had invested in highly risky assets, such as MBS, which were likely to fail.

In 2023 we are dealing with duration risk: The banks are holding “super safe” assets, such as Treasuries, that will most likely pay all of the promised money if held to maturity. The problem is that due to various factors (caused by wrongheaded fiscal and monetary policy), the bank might be forced to sell those assets before maturity at a substantial loss.

This is essentially also the explanation, why all of the recent stress tests of banks have not raised any concerns. As it turns out, apparently none of the stress test scenarios envisioned an environment of rising interest rates that turn Treasuries into dangerous assets — what an irony 🤡🤣.

For some for me unexplainable reason, people keep trusting in government initialized financial regulations, even if they prove time and time again to not prevent anything and instead usually make things worse, or at least lead to a faulty feeling of safety.

Where are we heading now?

All of these problems that SVB had, are not unique to them. They have just be the one domino most prone to topple first. All of the events that have happened are just the next dominos to fall as a consequence. The general problems spread throughout the entire economy and it remains to be seen, whether the current measures that have been implemented are able to contain the contagion from spreading further.

As stated above, essentially all banks are theoretically bankrupt when a certain threshold of depositors withdraws their deposits. At the moment there are many opportunities for investors to employ their money more productively (and potentially more safely) in other fixed income assets such as money market funds and by purchasing government bills and notes. As more people come to this realization, it could lead to draining out more money of the banking system and instead poring in to these alternatives, which in turn would lead to further havoc throughout the banking industry.

In addition, the stupid measures implemented by the government in response to the crisis already are — as always — creating the next problems and wrong incentive structures:

So far, the rhetoric has been that the government is not going to insure deposits beyond the FDIC limit in every bank, but rather just in those that are deemed critical for the system. This is basically telling everyone who has large deposits in a small bank to withdraw their money and put it somewhere else instead.

Thus, it is very likely that we will see bigger banks growing and smaller banks decreasing. More centralization. Just another unintended consequence of government intervention.

The newly established lending facility encourages banks to gain liquidity through giving the Fed their Treasuries which are currently at a marked-to-marked loss. This will spread the total underlying risk even more throughout the whole financial system.

“Variations also act as purges. Small forest fires periodically cleanse the system of the most flammable material, so this does not have the opportunity to accumulate. Systematically preventing forest fires from taking place 'to be safe' makes the big one much worse.”

— Nassim N. Taleb (in Antifragile: Things That Gain from Disorder)

Due to this environment a further aspects to keep an eye on is that the banking industry is likely more relient to give out loans at the moment, which of course has an important influence on the whole economy. Furthermore, it is not only the banking industry that has Treasuries on their books. Thus, watch out for foreclosures, defaults, layoffs, write-downs, restructurings and bankruptcies.

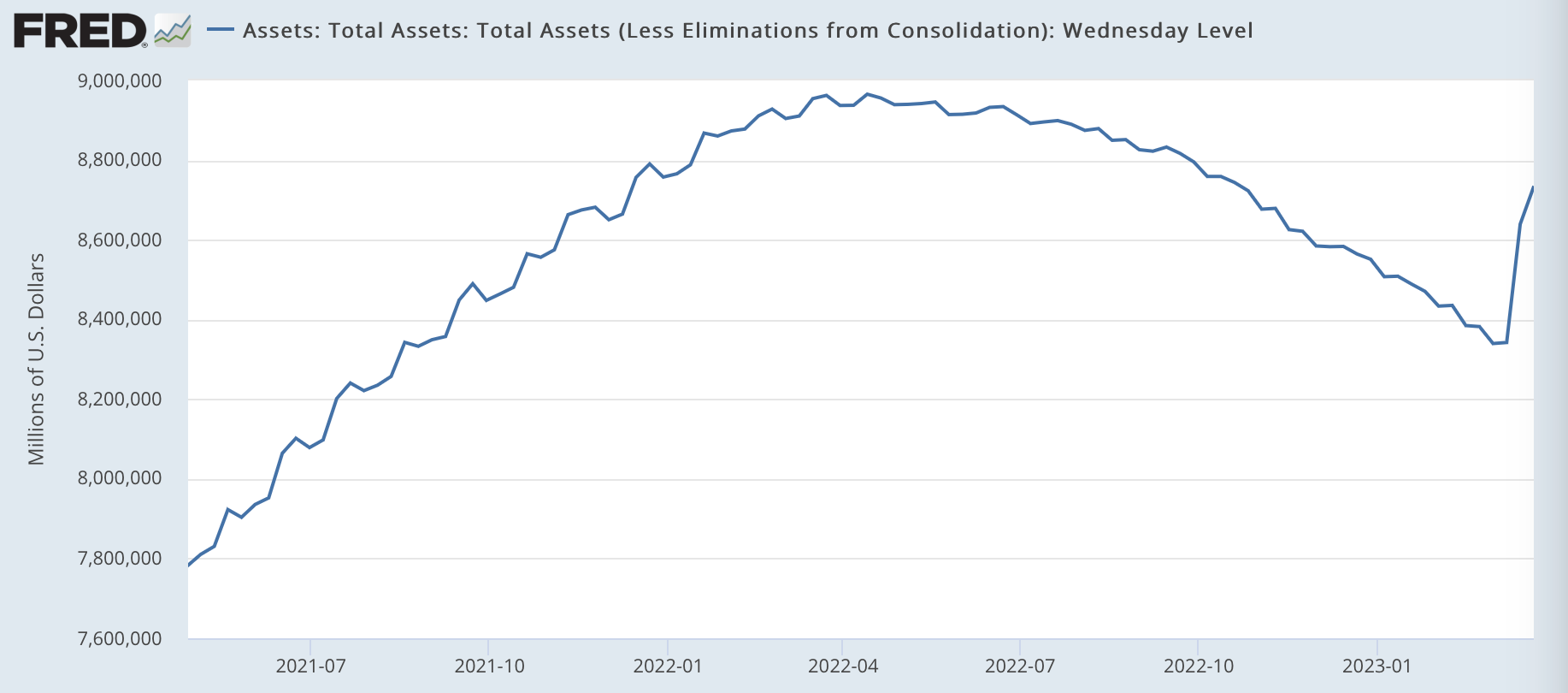

Finally, closing the circle, here is the balance sheet of the FED. This intervention has caused a substantial spike and basically unwound more than half of the balance sheet reduction that has occurred over the previous months. My guess is that we will see more of it:

If we zoom in a little bit and only focus on the last 1.5 years, the chart looks like this:

Let me one more time re-post the Mises quote, so that it sinks in:

"There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved."

— Ludwig von Mises

Do you think that we are going to take the road of “voluntary abandonment”? Leading to a widespread bankruptcies, massive unemployment, the collapse of our social welfare states and a substantial decline in the general standard of living that most western societies have come accustomed to and take for granted?

I don’t think so. Thus prepare for more money printing! 🤑

Portfolio Considerations

As for asset allocation and a healthy portfolio, I think now is the time to generally shift a bit away from cash and more towards hard assets again. And I also think it is a good time for increasing holdings in emerging markets and energy stocks again.

But shifts should be made carefully, it’s still possible that tightening continues a bit longer. It’s just that I think the likelihood of the printing presses running hot again has significantly increased.

And don’t forget to have — at least a small amount — in Bitcoin. 🚀

It will be interesting to watch how it all is going to play out. Stay tight!

I hope you enjoyed reading this newspaper. Likes, comments and shares are highly appreciated. I put a lot of work into it and if you think the content is worth your time, please consider to subscribe, so you can receive it on a monthly basis. Its free and without commercials.

Best regards,

Disclaimer: The content of this newsletter is for informational and educational purposes only. It contains my personal views and opinions, which are not to be taken as direct investment advise. All investments have risks and you should do your own due diligence before making any investment decision. If you require individualized advice, to review your unique situation and make a tailored advice for you, then contact a certified financial planner or other dedicated professionals.