Ataraxia Financial Newsletter - October 2023 Report

Ataraxia Financial Newsletter - October 2023 Report

The Ultimate Fate of All Fiat Money and the Potential Solution!?

“I don’t believe we shall ever have a good money again before we take the thing out of the hands of government, that is, we can’t take it violently out of the hands of government, all we can do is by some sly roundabout way introduce something that they can’t stop.”

— F.A. Hayek, 1984

Friday, November 3rd., Taipei, Taiwan.

Last month we examined the debt spiral that the United States finds itself in and we concluded that mathematically it is basically impossible to get out of it. Besides some (unrealistic) sudden innovation that boosts economic growth magnificently, there is just no chance of solving this issue in a way that does not include one of the following two options:

Very high inflation for many years.

Substantially cutting government spending across the board.

We also took the assumption that given the political landscape, the scope of spending cuts that would be required (actually any spending cuts) are unfeasible.

But in any event, in both cases, the standard of living for the majority of the people will have to go down a few notches.

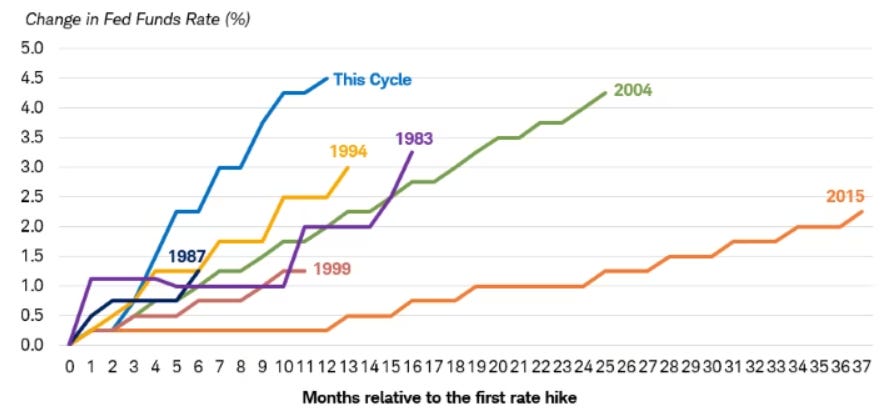

So far, over the last two years the Fed has been on a tightening path, to honor its official mandate and reign in inflation. To do this, it has raised the Fed Funds Rate at the fastest pace (at least percentage-wise) in its history:

We have been surprised by how determined the Fed has kept up with its hikes and how resilient the economy has handled the higher rates so far.

However, while there are many analysts who give credit to the Fed for succeeding in bringing down the inflation, we think that this credit is premature, given that inflation is still 85% above its target rate of 2% (and it’s reasonable to assume that the official CPI is tending to understate the real level of inflation).

Now, the Federal Funds Rate sits at 5.25% to 5.5% and Powell is indicating that there might be one more hike coming this year, which would bring it up to almost 6%.

In this newsletter we have repeatedly emphasized, how important the interest rate is for everything that is going on in the economy, it is the one price on which everything else depends. It’s interesting that it is not discussed more across the financial world and only recently got some more attention.

Here is what Howard Marks recently said in an interview:

To promote discussion these days, I often start by asking people, “What do you consider to have been the most important event in the financial world in recent decades?” Some suggest the Global Financial Crisis and bankruptcy of Lehman Brothers, some the bursting of the tech bubble, and some the Fed/government response to the pandemic-related woes. No one cites my candidate: the 2,000-basis-point decline in interest rates between 1980 and 2020. And yet, as I wrote in Sea Change, that decline was probably responsible for the lion’s share of investment profits made over that period.

At Ataraxia, we fully agree with Marks. Furthermore, we strongly believe that most of the major (negative) trends we have seen, such as the continuous rise in debt-levels, ever increasing bubbles in housing and stock markets, the rising gap between rich and poor, and a generally more short-term thinking in consumer behavior, is all a direct result of artificially depressed interest rates.

Moreover, even (allegedly) free-market promoters are seemingly unaware — or neglectful — of the fact that the most important market price is constantly being messed with in a “communist committee style” by central banks. This centralized micromanagement of the interest rate is the mother of all economic evil.

Given the continuous signaling by the Fed to keep course of its determination in the tightening cycle and the increased realization among market participants that interest rates might be staying high longer than most expected, the 10-year Treasury Rate has been hitting new heights, even briefly surpassing 5%.

We hold the assumption that an economy that has become addicted to low interest rates (or in other words: cheap money) is going to have a hard time to survive without it and — just like a drug addict — a withdrawal will be painful.

Thus, as the rates stay high, we are going to see defaults. Especially those entities that have taken on leverage and/or have financed themselves with short-term loans which have to be refinanced. For instance, basically the whole banking system is probably already insolvent if the they would be required to sell their treasury and mortgage holdings at current market prices and couldn’t use them as collateral at par value to get loans, as was established in the Bank Term Funding Program (BTFP) earlier this year when some banks collapsed (which is in essence just another form of QE).

The important assumption is, that the Fed will at some point be pressured to pivot (either by itself or through political pressure from the White House) and start enormous money printing — at a magnitude we have not seen yet!

What does that mean for the rest of the world?

The world is complex and complicated, but there are some principles that apply across the borders.

One of them is that all fiat currencies have the same fate — which is that they constantly lose value over time and eventually all of them go to zero.

It depends on the methodology to look at it, but according to Forbes, the average lifespan of a fiat currency is 27 years.

Now, some will say that a lot of currencies have been around far longer and that is true. But it also has to be considered that most of the currencies, which indeed have existed a lot longer, have undergone some substantial changes, huge devaluations, or hyperinflation, which basically can be considered as a restart.

Remember for instance that the dollar has only become a true fiat currency in 1971. Before that, it was (at least in theory) directly linked to gold. So it is “just” about 52 years old. For anyone who likes things being described by charts, there is a wonderful website to look at. For everyone else, the short story is that the un-tethering has led to a lot of unhealthy processes across the economy and an increased rate of decline in the U.S. dollar.

The dollar has been losing a lot of value, but it is still the king when it comes to fiat currencies, most other currencies don’t make it that far.

For instance, we are currently seeing hyperinflation-like atmospheres in Lebanon, Argentina, Turkey, Venezuela and Zimbabwe.

And I also highly doubt that the Euro will get to celebrate its 50th birthday. It’s not even 25 years old and already in deep trouble.

We previously wrote about the Milkshake Theory in last year's August Issue. The fundamental argument of it is that since the USD is the reserve currency, in which most international transactions are settled in and which most countries hold as their reserve asset, it is also the currency that will be popped up when there are any global market disruptions.

That is essentially what we assume is going to play out. So far we have not witnessed any major country experiencing hyperinflation-like situations, but given that they are all in a similar debt-spiral and are likely going to try printing their way out of it, we assume that the USD — as bad as it is — has a high chance of being the last domino to actually tumble.

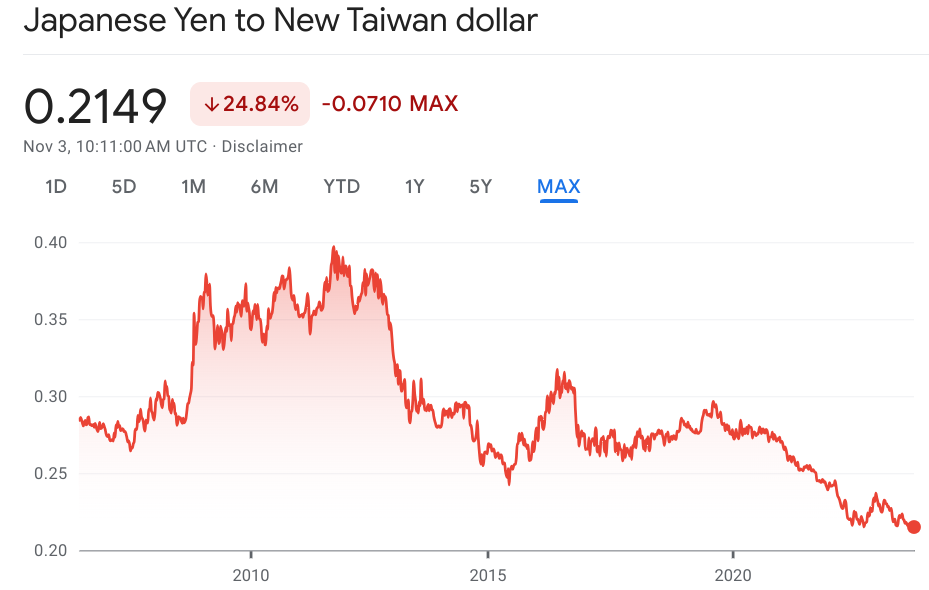

We have previously written about the situation and enormous debt levels in Japan (See part l here and part ll here). The Japanese Yen has long been considered as the ultimate save-haven currency. It does not look so rosy as a save-haven anymore. In November the JPY made another low in comparison to the USD.

Japan’s debt to GDP level stood at 263% at the end of last year.

An often mentioned study by Hirschman Capital pointed out, that out of 52 countries that reached government debt levels of over 130% of GDP, 51 ended up defaulting on the debt within the next 15 years in some way or another. So far Japan is the only country that has been able to defy this disaster event — so far.

However, unless Japan can manage to decrease its debt, it cannot be called a success and the likelihood that they will be able to pull it off is diminishingly low.

Hence, in consideration of Japan's enormous debt level and the upward pressure in interest rates, the Japanese central bank is likely gonna be required, to purchase most of the government bonds in order to keep the interest rates in check (at around 4% all of Japanese tax receipts would be required just to service the debt). How does the BOJ buy those treasuries — with freshly printed money of course. Thus, the JPY is destined to head lower — even against a value-loosing USD.

Why do these fiat currency always decline?

Well, dear reader…

A financial system based on credit is just an exchange of money today for money later. I give you dollars today and temporarily lose the utility of my money in exchange for having more later. You have the inverse: the benefit of more money today and less tomorrow as you pay back the loan with interest.

This system works on trust – trust that you will pay back what you said you would pay. It is the same whether that trust is in a person, company, or government. Remove trust and it affects the credit-worthiness of an individual or company. Remove trust from a system and the entire system can unravel very quickly.

— Jeff Booth (The Price Of Tomorrow)

…And we are back to our favorite culprit: The state.

The state has — by force — overtaken the control of money. That’s why almost every country has its own fiat currency.

The incentives that come with being in control of money and being able to generate it, is just such a strong and perverse incentive, that it is impossible to resist it.

Especially when we consider how these incentive structures are at work in the ever growing governments of our “Western Democracies”, which have literally grown like weed.

Any politician who wants to have a shot has to promise something to “give” to “his”or “her” people. And it is quite easy to offer something that you don’t have to earn by yourself. That is the main reason why we see the bureaucratic welfare states grow and grow. Realistically, most Western governments already charge over 50% in taxes. People usually just think about the personal income tax, and will argue that it is not that much, but that is only one part of it. There are several other taxes which either directly or indirectly also affect the standard of life for everyone. Some of them are:

VAT tax (in many countries around 20%).

The corporate tax (the check might be written by the corporation, but make no mistake, the working people are the ones who are really paying for it in one way or another).

Inheritance tax (varies a lot but can also have a significant effect).

But even those are not enough for the growing government cancer. The most dishonest and insidious tax of them all is inflation.

Yes, inflation is a tax. It is the indirect result of printing money to finance government debt.

As we become more efficient and our economies grow, the natural outcome should be a reward in the form of constantly falling prices which allows a higher standard of living. The reality is the opposite.

This tax is the most dishonest and stealthy, as it allows politicians to spend more than they generate through direct tax generation, but instead by deficit spending. The consequently resulting inflation can later be blamed on any other current affairs that are going on (such as Putin, climate change or greedy capitalists) and the majority of the population does not grasp the direct connection between government spending and inflation.

The most important thing to remember is that inflation is not an act of God, that inflation is not a catastrophe of the elements or a disease that comes like the plague. Inflation is a policy.

— Ludwig von Mises

We are aware that we singled out the western democracies here, but the base case is a simple rule that throughout history so far has always held true:

→ A government with the tool of money creation will always use it.

To conclude, like Hayek stated all the way back in 1984, if we ever want to have sound money, we have to take it away from the government.

So what is the solution?

Most readers of Ataraxia will probably know the answer already.

Gold has long been the money that was naturally chosen by people because it best fulfilled the properties required to be a good money.

However, it had its shortcomings because:

it is slow and difficult to transfer over space.

it is not very convenient to verify.

it can be confiscated and is difficult to transport across borders (especially since the metal detector was used at airports).

Those facts have led to centralization, which in turn made it possible for governments to control and finally de-pegg it from its fiat currency.

With Satoshi’s invention of Bitcoin back in 2008, a form of money has entered the space which a) has all the positive properties that made gold the chosen commodity to become the money of choice and b) it does not have the shortcomings listed above.

Thus, coming back to Hayek’s quote:

“…all we can do is by some sly roundabout way introduce something that they can’t stop.”

→ Bitcoin!!!

We started this report by talking about interest rates of Treasuries. They are generally considered the safest investment to make. Bitcoin on the other hand is considered as a high-risk asset. Well, Treasuries have lost more value from their all-time heights than Bitcoin. It begs the question whether Treasuries are such a safe investment after all. Holding them resulted in a loss of over 50% denominated in a value-losing currency. If that is considered investment safety, then what should be considered risky?

In our opinion, Bitcoin has high short-and-medium-term risks in terms of price volatility, but from a long-term perspective, it is a way more secure investment.

One of the most baffling things about the world of finance is how few of the financial commentators, investors and other “experts” have grasped the concept and value proposition of Bitcoin. These should be the smartest people who have spent years and careers in studying markets. And nonetheless, they seem incapable of even critically analyzing this asset in a honest and curious approach with the goal to get a clear understanding of what it is and why it has not disappeared after several hype and bust cycles, although it is literally looming above the financial world with big written letters.

Instead they still just give a disregarding smile when the topic comes up and maybe talk about the value of “cryptocurrencies and potential future innovations through blockchain technologies”, some might recommend to buy a small percentage for speculative reasons, but almost none of them has any idea of what that asset really is.

They do not understand that the real innovation has already happened, and it is Bitcoin, not crypto.

One of the exceptions is Jurrien Timmer, who is the Director of Global Macro at Fidelity. He understands the value proposition and in a recent tweet he stated:

“In my view, Bitcoin is a commodity currency that aspires to be a store of value and a hedge against monetary debasement. I think of it as exponential gold.”

And he posted the following chart, which everyone interested in investment should analyze, study and deeply think about the reason for this price development, its validity and the implications of it:

In the next issue we will look once more a bit closer on how Bitcoin is likely to become an increasingly held asset over the coming years, that subverts the current financial system and has a good shot at establishing itself as a global store of value and trustable underlying settlement system — by irresistible voluntary adaption.

Stay tuned.

P.S. This time I didn’t write anything about what I am currently up to in the beginning, but I am enjoying my time in Taipei a lot. Here is a shot from my favorite spot in the city. The view of the Taipei 101 (which held the title of the worlds tallest building from 2004 - 2010) and the surrounding modern and lively Xinyi District.

I hope you enjoyed reading this newspaper. Likes, comments and shares are highly appreciated. I put a lot of work into it and if you think the content is worth your time, please consider to subscribe, so you can receive it on a monthly basis. Its free and without commercials.

Best regards,

Disclaimer: The content of this newsletter is for informational and educational purposes only. It contains my personal views and opinions, which are not to be taken as direct investment advise. All investments have risks and you should do your own due diligence before making any investment decision. If you require individualized advice, to review your unique situation and make a tailored advice for you, then contact a certified financial planner or other dedicated professionals.

View draft history

Settings