Ataraxia Financial Newsletter - September 2023 Report

Ataraxia Financial Newsletter - September 2023 Report

Treasury Rates Soar, Boosting the Debt Spiral - Brace for Impact!

"The budget should be balanced, the treasury should be refilled, public debt should be reduced, the arrogance of officialdom should be tempered and controlled, and the assistance to foreign lands curtailed lest Rome become bankrupt."

— Cicero, 63BC

Tuesday, October 3rd., Tainan, Taiwan.

I am back in Tainan, which is a very unique city in the southern part of Taiwan. I called it my home for 5 years and I still feel a special attachment to the unique vibe and atmosphere of this city.

So I am really enjoying my time here and going to all the familiar places again — and the seaside is just perfectly located for enjoying sunsets! 🤩

That’s also my excuse for publishing this report a bit late. 😅

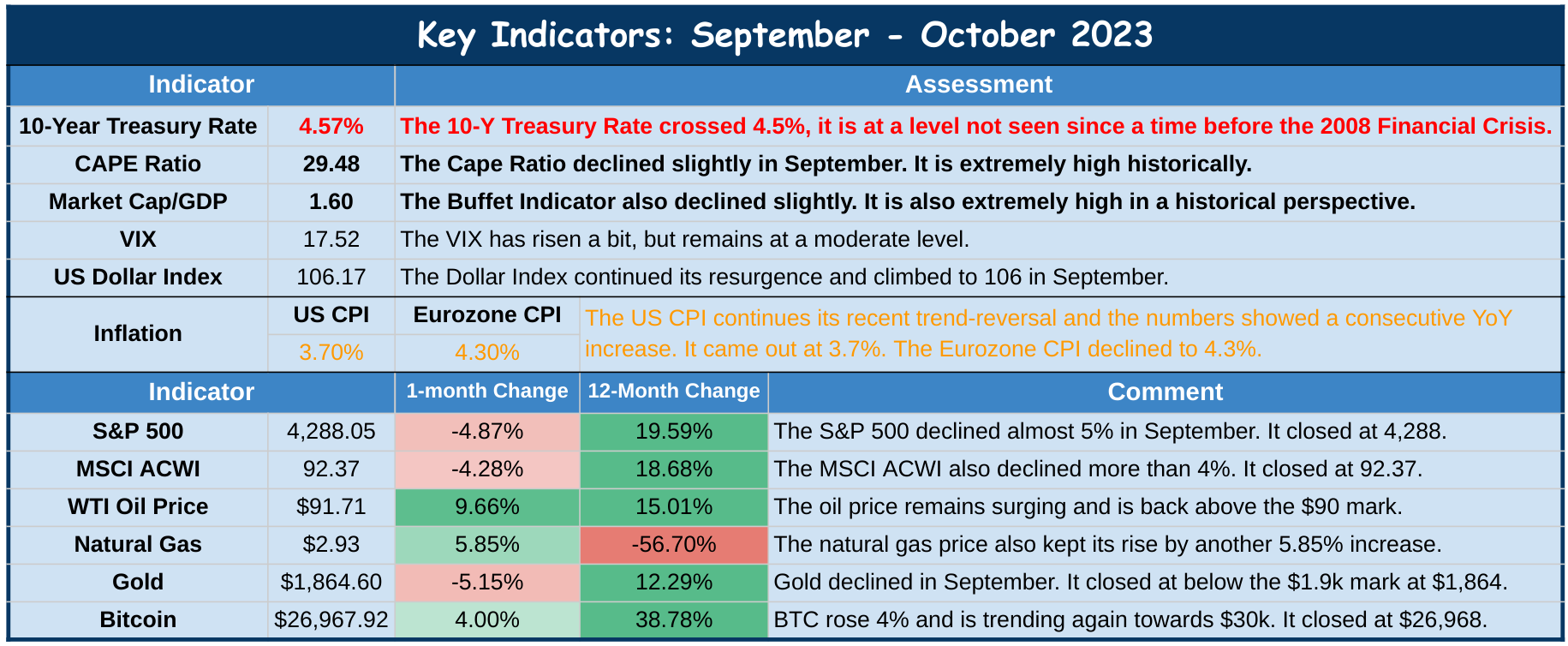

Here are the Key Indicators for September:

The most important number underlying the whole global economy is the 10-Year Treasury Rate. As you can see, it is now above 4.5% tending higher. I made it bold and marked it in red.

I wrote about why it is so important extensively in the February 2022 issue. Here is an excerpt of it:

If I would be asked to pick only one indicator, to determine what is going on in the markets, I’d choose the 10-year Treasury rate. I think it is the most determining factor in the economy.

First, it is probably, next to the S&P 500, the mostly watched number in finance. Therefore, it serves as a comparison parameter for all other bond rates. In addition, it also serves as a proxy for mortgage rates. Furthermore, Treasuries have the highest market capitalization of all bonds and are also the most liquid. Having this in mind, the total market capitalization of the global bond market (estimated at around $120 trillion), dwarfs that of any other asset class. There is also an argument to be made that they are a gauge for the general investor confidence, as its moves provide a hunch at the perceived overall risk in the market. Lastly (and maybe most crucially), it is usually considered as the risk-free rate, hence, it is used for determining the economic viability of long-term business projects, as well as stock valuation.

As readers should be aware by now, the key assumption of this newsletter is that our financial system is thoroughly flawed and that the reason for it is that it relies on fiat money. The whole global economy depends on money that can be manipulated and created “out of thin air” by the whim of authorities. Furthermore, the backbone of international trade is the U.S dollar and therefore U.S. Treasuries have become the global reserve that links everything else together. Thus, it follows that the main culprit for everything that’s going wrong in the economies around the world is the unholy alliance between the U.S. government and the Federal Reserve.

However, if a parasite gets too greedy, grows too quickly in comparison to its host, it is destined to run into trouble at some point. This is the basic conceptualization of what we are seeing. Governments and its related institutions are the parasites and the private sector that is actually producing the things that are required for life and produce the goods and services which make it pleasurable is the host.

The debt spiral that we have been talking about seems to be speeding up and rising Treasury yields are boosting the process:

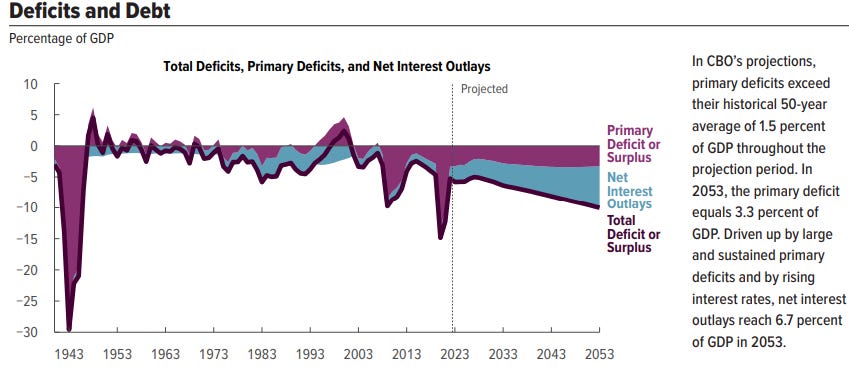

Here is a chart that was published in a report that was published by the Congressional Budget Office itself, just a few months ago:

As you can see, the main factor here are the increasing net interest outlays, which should make it obvious, why the Treasury yield is so crucial. It takes some time for the debt to roll over, but If the debt burden is small, higher rates hurt, but they might be managed. The U.S. — and most other countries — are far beyond a manageable deficit!

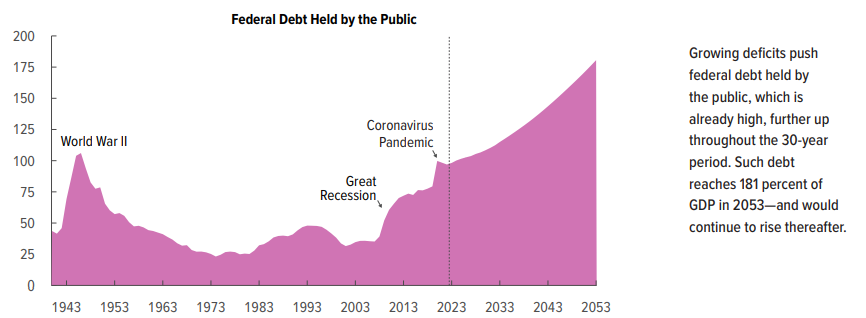

And here is how that looks in a prediction of the total debt level as a percentage of GDP.

Quick Note: This report was published in June and just 3 months later we are already notably “ahead of schedule”.

Moreover, all of their forecasts are made under the assumption that there are no recessions or events such as pandemics or wars, which would undoubtedly result in additional government outlays and deficits.

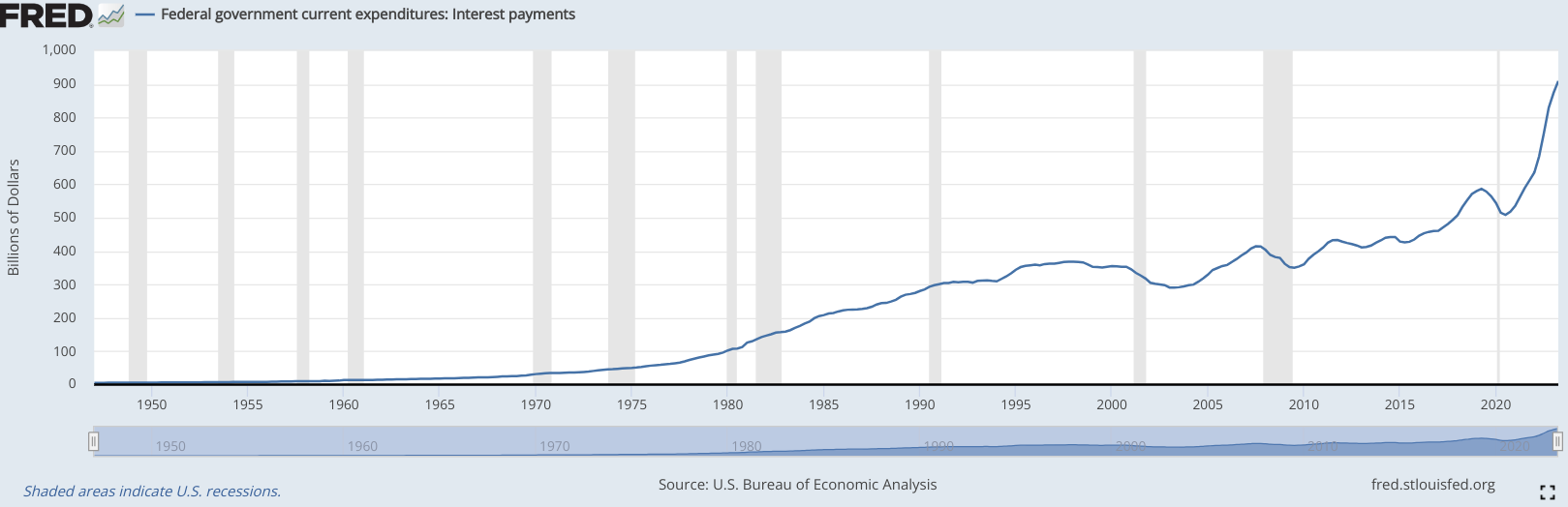

But coming back to the interest rate, here is the chart that shows the government net interest payments:

The extreme rise is directly related to the increase in the Treasury rates over the last 2 years and it is compounded by the huge additional deficits that are on an exponential trend. The debt is financed by Treasuries of differing maturity lengths, but as they mature, they have to be refinanced. Without going too much into the details, the baseline is that a $33 Trillion deficit financed with Treasuries of a 4.6% interest would require a yearly net interest expense of over $1.5 Trillion. So that's where the above chart is headed at current rates. That’s about 40% of the total government revenue.

Even without any net interest payments, the U.S. The government would be required to go into deficits to cover all its promises and operations. Taking the interest into account the total deficit spending is currently running at around 8.5% of GDP.

The current prediction is a GDP increase of 2%. Which means that without the government deficit spending, the economy would actually decline by about 6.5%. If that would happen, the revenues would also take a magnificent hit, while all the cost would remain, or actually substantially increase.

In other words… the U.S. government is bankrupt.

And the only reason that they don’t file for bankruptcy is that everybody knows that they theoretically have the power to print as much as they want to bail themselves out.

Well, then what are the parastits options to proceed…

Option A) Balancing the Budget

This would require to cut about 1/3 of the government expenditures immediately.

Social Security

Health

National Defense

Medicare

Income Security

Those are the largest line items in the budgets except for net interest and therefore large cuts in all of them would be necessary.

I think everyone who pays only small attention to political affairs knows that the likelihood of this option is 0%.

Option B) The Continuation of Massive Deficit Spending

This is the obvious way I think it will play out. The important aspect from an investment perspective is that it requires massive debt financing and I think as the debt-spiral situation is becoming more and more obvious around the world, it will be reflected in continuous upward pressure in the Treasury Rates. As that happens the FED will be more and more cornered and finally will be forced to massively intervene with QE or in some other way of money creation, to prevent the Treasury market from totally spinning out of control.

We have mainly focused here on Treasuries and how the treasury market is directly linked to the U.S. deficit. In the next issue we will analyze how this all connects to the rest of the world.

In short, while we U.S. government and the Federal Reserve as the main culprits for the disastrous fiat money scheme, the U.S. Dollar is most likely not the first major stone to tumble. Amidst all of the financial trouble and inflation, the U.S. Dollar Index has recently been rising against all other major currencies.

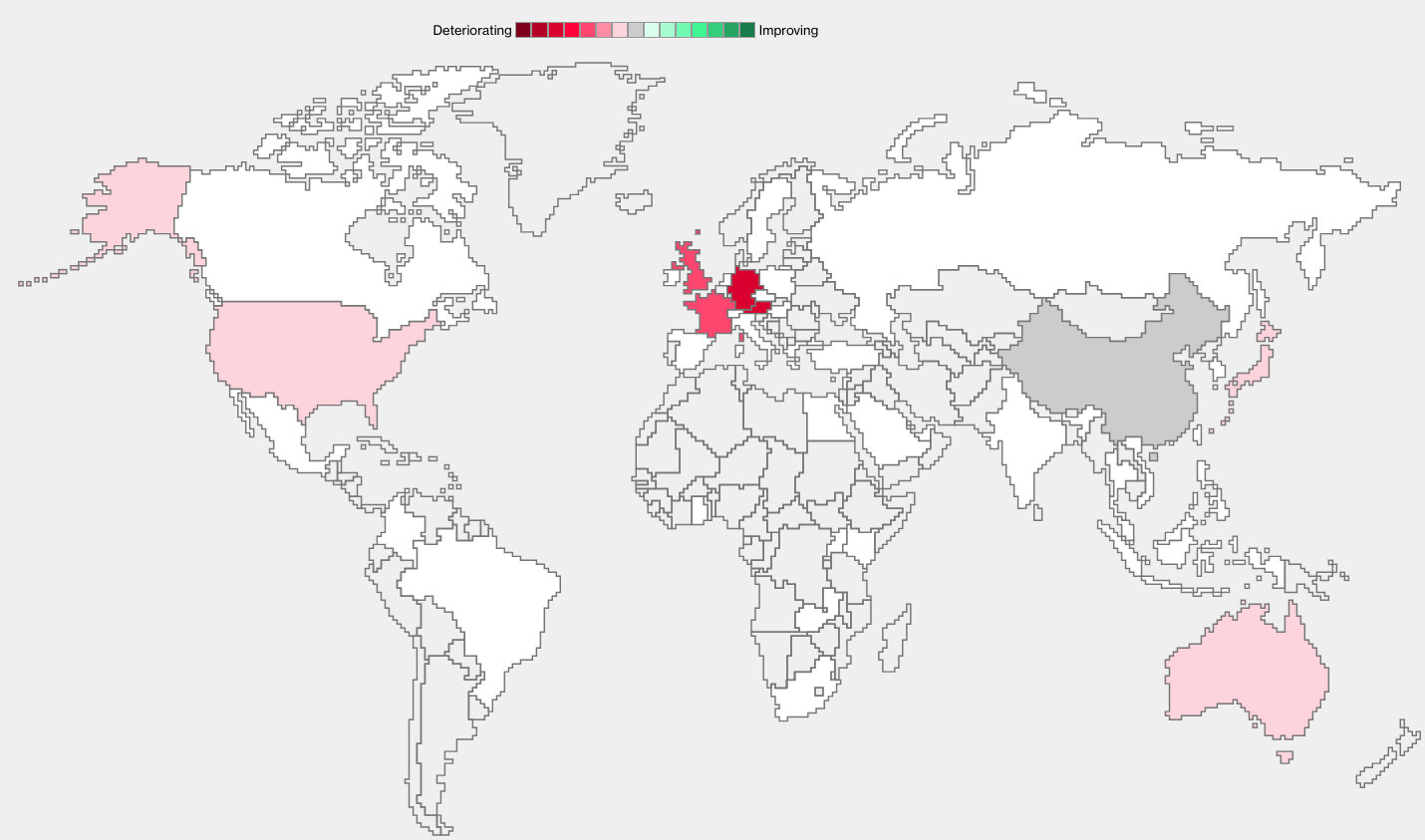

And here is a quick forecast:

The PMI is an indicator that provides insights into the health and direction of a country's manufacturing sector. It is not looking good for all the major countries that drive global production, especially central Europe.

And recent statistical metrics have confirmed that Germany has just entered a technical recession.

We will try our best to connect the dots and try to get a better understanding of how this all works together.

Stay tuned…

I hope you enjoyed reading this newspaper. Likes, comments and shares are highly appreciated. I put a lot of work into it and if you think the content is worth your time, please consider to subscribe, so you can receive it on a monthly basis. Its free and without commercials.

Best regards,

Disclaimer: The content of this newsletter is for informational and educational purposes only. It contains my personal views and opinions, which are not to be taken as direct investment advise. All investments have risks and you should do your own due diligence before making any investment decision. If you require individualized advice, to review your unique situation and make a tailored advice for you, then contact a certified financial planner or other dedicated professionals.